OKR >

Balanced Scorecard (BSC) explained simply

The Balanced Scorecard is a powerful tool for companies. It ensures continuous optimization in strategic management and helps to minimize risks and promote long-term competitiveness. The balanced scorecard model is a good way for companies to remain successful on the market in the long term. It also provides a balanced basis on which the development of the company and the implementation of the company’s strategic goals can be rolled out.

Inhalt

verbergen

OKR (Objectives and Key Results) – successor or supplement to the Balanced Scorecard

We, the OKR experts, will be happy to support you with the introduction of OKR. The introduction of the OKR can take place in combination with the Balanced Scorecard or as its further development, i.e. as a replacement. The balanced scorecard and the perspectives of the BSC can continue to serve as a source of inspiration for the OKR sets.

- Field-tested implementation process

- Avoid mistakes, reduce effort

- Manage the coexistence of BSC and OKR correctly – or replace BSC with OKR

- Top rated seminars & workshops

- Support in selecting an OKR tool

What is the Balanced Scorecard – BSC all about?

This article deals with the basic idea of the Balanced Scorecard as a management system, as a management tool. In addition, four different perspectives are explained that make up the basic function of the BSC. The advantages and disadvantages of using the system are also discussed. Lead and lag indicators then provide information on a supporting extension of the BSC.

The tried-and-tested seven-step plan is explained so that the BSC can be applied immediately in practice. This offers specific instructions and guidelines for creating a BSC – including a practical template to download and a concrete example.

The article then shows how the OKR method can further increase the efficiency of the BSC in order to implement strategic goals – or how the BSC can enrich the OKR method to identify strategic goals (strategy mapping, strategic management).

The article is rounded off with an FAQ at the end.

Balanced Scorecard definition and initial information on the concept

The Balanced Scorecard (BSC) is an instrument used in strategic management. Specifically, it helps companies to visualize goals, measure their own performance and track progress. Important key figures, such as KPIs (Key Performance Indicators), can play a role here. It can also help to increase employee satisfaction and minimize the number of customer complaints.

The Balanced Score Card is a concept in performance management. It is about evaluating the performance of a company not only on the basis of financial key figures. If a company concentrates solely on its economic situation, valuable potential is lost. In addition to the financial result, the BSC considers the perspectives of “customers”, “internal processes”, “learning and development” and their interrelationships.

Why Balanced Scorecard? – Implementing strategies correctly

The balanced scorecard stands out due to its focus on a balance between financial and non-financial key figures. This also explains the name of the system – the focus is on a holistic and balanced assessment of the company’s performance. To this end, the key figures of the various perspectives are kept in balance. The BSC thus offers an effective method for company management to successfully implement its business strategy and achieve long-term success.

And who invented it? Kaplan and Norton

The Balanced Scorecard was developed at the beginning of the 1990s by the economists Robert S. Kaplan and David P. Norton.

The four perspectives of the Balanced Scorecard

The BSC is defined by one central feature: it considers four perspectives that enable a comprehensive assessment of the company’s performance. It is not just profit or returns that count: the traditional financial spectrum is being expanded to include non-financial indicators. The balance of the following perspectives is important for the function of the BSC:

- the financial perspective

- the customer perspective

- the process perspective

- the learning and development perspective

The individual perspectives are discussed in more detail below.

Perspective #1: the financial perspective

The financial perspective is one of the fundamental pillars of the Balanced Scorecard. It focuses on the financial targets and quantitative resources of a company. This includes key figures such as:

- Sales growth

- Profitability

- Cash flow and

- Shareholder value.

These key figures enable sectors to measure their financial health and profitability (“financial performance”). In addition, strategic ambitions to optimize the value of the company should be achieved and potential risks identified at an early stage, for example to avoid a reduction in profit.

The financial perspective is central to the use of the balanced scorecard

Perspective #2: the customer perspective

The customer perspective must also be taken into account when applying BSC.

The customer perspective creates an awareness of the needs and expectations of customers. Companies must take their reactions into account and adapt to them in order to achieve long-term customer loyalty and thus competitive advantages. Key figures such as

- Customer satisfaction

- Customer relationship

- Market share and

- Service quality

are relevant for successful cooperation.

Consequently, it is of great benefit to companies to evaluate their own performance from the perspective of their customers. Employees often provide valuable input. In addition, offers can be continuously tailored to customer preferences.

Perspective #3: the internal process perspective

The process perspective deals with the internal processes and developments of a company. The focus here is on key processes that visibly improve the efficiency and quality of the company (“business processes”). An examination of the corporate strategy Indicators such as

- Throughput times

- Error rates

- Productivity and

- Ability to innovate.

These enable companies to identify weak points and respond to deviations in a targeted manner. The process perspective makes it possible to reduce costs, make qualitative progress and thus increase customer satisfaction.

Ongoing processes must be monitored to ensure a successful process.

Perspective #4: the learning and growth perspective

In order to achieve success, further training must be provided on a regular basis.

The learning and development perspective focuses on the company’s own skills and the qualitative resources in the industry. The continuous development of professional skills is essential for the progressive growth and long-term success of a company.

In concrete terms, for companies this means investing in the (further) training of employees, especially in skilled workers. This enables a functional infrastructure, ongoing staff motivation and the augmentation of specialist know-how. A satisfied workforce, consistent training measures and the resulting innovations are the key indicators for the learning and development perspective.

BSC hierarchy pyramid

Balanced scorecard advantages

The advantages of the Balanced Scorecard can be broken down into the following four points.

- A holistic view: The balanced scorecard enables a comprehensive measurement of a company’s performance and thus facilitates quality management, for example. This performance is made up of a large number of indicators – making the BSC a balanced reporting form. The BSC takes into account not only financial aspects, but also social and, depending on the planning, ecological factors and success factors. This effectively counteracts a one-dimensional assessment of the company’s performance and creates a holistic picture.

- Strategic commitment: The balanced scorecard helps companies to define their strategic goals and implement them with measurable key figures. It enables the organization to focus on its strategic goals. It also promotes cooperation and coordination between different departments and teams. Ambitions regarding the sustainability of a company can also be integrated into strategic planning.

- Transparency through communication and measurability: The use of a balanced scorecard creates transparency about a company’s performance. This enables target-oriented communication both internally and externally. Strategic customer orientation and structured teamwork promote this transparency enormously. In addition, employees and stakeholders can track the company’s progress through the presentation of targets and key figures.

- The BSC as an early warning system: By integrating a balanced scorecard, potential problems can be identified and addressed at an early stage. The company’s performance is continuously measured and monitored. If deviations from the desired values are detected, appropriate measures can be taken in response. For example, a high sickness rate can be an indication of dissatisfaction among employees. However, sustainability indicators can also be successfully integrated and offer companies the opportunity to react to environmental conditions that cannot be influenced.

Balanced scorecard disadvantages

The following points can be seen as disadvantages of the balanced scorecard.

- Complexity: Implementing the Balanced Scorecard in management requires time, resources and a thorough understanding of your own corporate strategy. The development, elaboration and final integration of relevant key figures can prove to be a complex process. This is often the case, especially for industries with different business areas or a global presence. The more indicators are to be exposed, the more complicated their integration into the corporate structure becomes.

- Availability and quality of data: The successful use of the Balanced Scorecard is based on the availability of reliable data. If the validity of these is not guaranteed, data processing can become a challenge for companies. It is therefore important to set up a suitable system that provides accurate data content for measuring performance.

- Subjectivity in interpretation: The selection of balanced scorecard indicators is influenced to varying degrees by subjective assessments of employees. The interpretation of results can also lead to internal and external differences of opinion. A uniform interpretation of data is possible if the company can proceed according to defined criteria. These criteria should be developed through discourse and require a constant exchange of ideas within the team.

The Sustainability Balanced Scorecard

The Sustainability Balanced Scorecard is an extension of the traditional Balanced Scorecard. While the traditional Balanced Scorecard generally takes into account key financial figures, customer perspectives, internal business processes and learning and growth factors, the Sustainability Balanced Scorecard adds an additional dimension: sustainability. This expanded version takes environmental aspects, social responsibility and long-term economic stability into account and integrates them into the company’s strategic planning and performance assessment. This reconciles short-term profits on the one hand and long-term sustainability goals on the other. In this way, companies can strive for more holistic, responsible and ultimately more sustainable business management.

The following table provides an overview of the advantages and disadvantages of the SBSC.

| Vorteile | Nachteile |

|---|---|

| Ganzheitliche Betrachtung | Komplexität |

| Strategische Ausrichtung | Mangel an Standardisierung |

| Stakeholder-Engagement | Kosten |

| Risikomanagement | Interne Widerstände |

| Innovationsantrieb | Kurzfristiger Fokus |

The SBSC provides a comprehensive understanding of the company, in which financial, social and ecological aspects are integrated. By integrating sustainability goals into the corporate strategy, the SBSC simplifies the alignment of all business processes with long-term goals. Taking sustainability factors into account also appeals to a broader range of stakeholders – from investors to customers and communities. This can improve the company’s reputation. The SBSC can also help to identify environmental and social risks at an early stage and take action.

On the other hand, the inclusion of several dimensions in the scorecard can complicate implementation and management. As sustainability covers a broad range of topics, there is often a lack of standardized measurement methods. This makes it difficult to compare performance over time or between companies. The development and introduction of an SBSC can also lead to high initial investments. Employees and managers may first have to be convinced of the value of incorporating sustainability aspects. Finally, due to the urgency of day-to-day business, the focus on the long-term goals of sustainability can be lost.

The SBSC is therefore a multi-layered tool with potential and challenges for its users. The introduction of the Sustainability Balanced Scorecard should therefore be carefully considered.

An article by Kaplan and McMillan – published in the Harvard Business Review:“Reimagining the Balanced Scorecard for the ESG Era” – is interesting in this regard.

OKR Trainings & Schulungen

Wir, die OKR-Experten, schulen Sie gerne mit unseren modernen Training-Formaten:

- Seminare in Präsenz & Remote

- Offene Schulungen & Inhouse-Seminare

- Workshops & Video-Kurse

Lead and lag indicators or key figures in the context of the balanced scorecard

Lead and lag measures are metrics for a performance measurement system. They are used, among other things, in the advanced use of balanced scorecard controlling. The combination of both indicators is intended to support the BSC and aims to ensure the long-term success of the company.

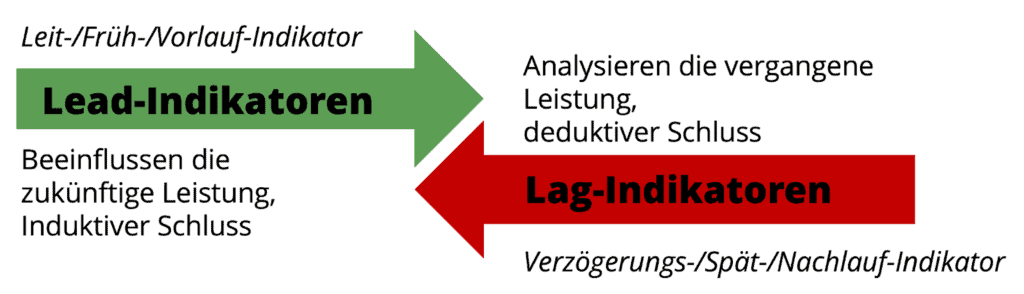

Lead indicators look to the future, lag indicators look to the past.

Lead-Measures – engl. Leading indicators – influence the future

Lead measures are forward-looking metrics. They are based on activities and processes that influence the future success of a company. Lead measures therefore figuratively describe the “path to the goal”. They enable reactions to potential deviations in this way, as the effectiveness of strategic measures can be permanently monitored. Lead indicators can generally be influenced and actively controlled.

In the context of the Balanced Scorecard, the success of a company depends primarily on the four-perspective model. The idea of lead indicators can now be illustrated using examples of the individual perspectives:

- From the customer’s perspective: regular customer satisfaction surveys before and after the sale are used to obtain feedback at an early stage. This identifies potential problems or areas for improvement. The surveys therefore describe an activity that influences the future success of the company.

- Based on the learning and development perspective: investments are made in staff development through regular training and further education measures. This increases professionalism and know-how in the team. This process influences the productivity of the company and thus also its long-term measured success. The “path to the goal” is thus metaphorically expanded.

Lag-Measures – dt. Lagging indicators – measure past success

Lag measures are retrospective measures. They are based on the results and services of a company that have already been completed in their process. Lag-Measures now puts the “path to the goal” in the background and the goal or the result itself in the foreground.

Lag indicators are used to evaluate the effectiveness of past measures retrospectively and to check whether targets have been achieved. Based on this, conclusions can be drawn for new upcoming processes and goals.

Lag measures can also be directly linked to the balanced scorecard using specific examples:

- From a financial perspective: The growth of a company’s sales can be measured and interpreted once a performance period has been completed. The evaluation of past measures provides information on how successful the sales and marketing activities are proving to be.

- Based on the customer perspective: The success of a company in a completed performance period can be measured by the customer satisfaction index, among other things. This index is based on the evaluated surveys or on direct feedback from customers. It provides information on satisfaction with the company’s products and services.

OKR Seminar mit offizieller Zertifizierung zum OKR Coach / Master

Wir, die OKR-Experten, bilden Sie gerne zum OKR Coach / Master aus:

- in Präsenz & Remote

- Erlernen & Erleben der OKR-Methode

- Best Practices, Tipps & Tricks

Seven steps to introducing, developing and setting up a balanced score card

Following the seven steps makes the successful introduction of a balanced scorecard more likely.

- Definition of the company’s strategic goals:

This first step requires a central vision, a leitmotif. This should enable the industry to define itself. Objectives should be specifically identifiable and reflect the strategic priorities. Examples of such targets are sales growth, customer satisfaction or product innovation, but they can also be selected individually. - Selection and prioritization of relevant perspectives:

The typical perspectives for the BSC include finance, customers, processes, learning and development and have already been explained in detail. However, these do not necessarily cover all aspects relevant to the company. They can be expanded to include the perspective of sustainability management, for example. - Definition of measurable goals:

Specific aspirations should be defined for each perspective according to the so-called SMART criteria. SMART is an acronym for specific, measurable, achievable, realistic and time-bound. For example, a company may decide to increase sales by y % in the next x months. - Identification of suitable key figures:

Appropriate key figures should be selected for each perspective to serve as measures of overall progress. The team should be guided by these key figures and recognize a direct link to the previously defined goals. From the customer’s perspective, one such indicator could be the so-called Net Promoter Score (NPS). This measures customer satisfaction. - Definition of target and threshold values for the individual key figures:

Target and threshold values are again set for the key figures defined in step four. Target values indicate what performance is aimed for with the respective key figure. Threshold values determine the limits above which the team must react to a drop in performance. - Visualization of the scorecard:

In order to make the scorecard comprehensible, it should be visualized in the form of a table or dashboard. A clear presentation of the relevant perspectives, objectives, key figures and values is self-explanatory for successful development. - Implementation of the BSC:

Finally, the scorecard is integrated into the company’s organizational processes and communication channels. The better the employees’ understanding of the topic, the easier it is to integrate the scorecard. The new system must be regularly reviewed and possibly adapted, especially during the “familiarization phase”.

An example of a balanced scorecard

The balanced scorecard is illustrated below using a simple example. The scope of the example has been deliberately kept manageable to facilitate understanding. It does not serve as a benchmark for a sophisticated scorecard.

Financial perspective:

- Target: Increase net profit by 15 % in the next financial year.

- Key figures: a) Sales growth, b) Gross margin, c) Operating cost ratio, […].

- Target and threshold values: for a): e.g. 5 % as a target, 3 % as a threshold, […].

Customer perspective:

- Goal: Increase customer satisfaction to 90%.

- Key figures: a) Customer ratings, b) Complaint rate, c) Repurchase rate, […].

- Target and threshold values: for b) e.g. “A maximum of 1/10 customers complain about the product” as a target, “At least 3/10 customers complain about the product” as a threshold, […].

Perspective of internal processes:

- Goal: Reduce throughput time by 20%, i.e. the company should be able to complete orders and other processes more quickly.

- Key figures: a) Lead time of process X, b) Number of errors in process Y, c) Efficiency rate, […].

- Target and threshold values: for a) e.g. “processing of a new order within 48 hours” as a target, “processing of a new order with a lead time longer than 72 hours” as a threshold, […].

Learning and development perspective:

- Objective: To promote staff development through regular training.

- Key figures: a) Training days per employee, b) Staff satisfaction, c) Staff turnover, […].

- Target and threshold values: for a) e.g. “At least three training days per employee per quarter” as a target, “one employee misses at least two training days per quarter” as a threshold, […].

Case studies with further examples can be downloaded from the website of the Balanced Scorecard Institute.

Can a balanced scorecard be used with OKR?

The “Objectives and Key Results” (OKR) method is establishing itself as another powerful tool in corporate management: as an agile strategy implementation method and modern goal-setting method. If the four perspectives of the Balanced Scorecard are used for OKR, a company can be further optimized in terms of its objectives and performance.

OKR – a digression

Objectives and Key Results is a framework for defining and pursuing objectives within an organization. The OKR approach aims to set ambitious and measurable goals (objectives) and define specific results-oriented metrics (key results) including target values. The key results are quantitative and measurable in order to be able to evaluate the result and progress towards the objective. An OKR set consists of an objective and several key results.

OKRs promote focus, alignment, alignment, commitment, transparency and motivation across the organization by ensuring that all departments and teams clearly understand their goals. In contrast to the Balanced Scorecard, which focuses on a balance between different performance criteria, the OKR approach concentrates on achieving specific and ambitious targets within a specific time frame, usually 3 months.

Articles about OKR

An article about OKR – Objectives and Key Results can be found here with the title“OKR Method“.

BSC and OKR – an integrated strategy for effective target management and optimal corporate governance

The four perspectives of the Balanced Scorecard: financial perspective, customer perspective, internal process perspective and learning and growth perspective offer a holistic approach to defining the organization’s strategies and thus also for the OKR objectives. They can be used to create high-quality, balanced OKR sets. For example, financial OKR targets could be set for sales growth or profit margins, while OKR sets from the customer perspective could set targets for customer satisfaction or market conquest. Internet-oriented OKR sets could aim to improve specific operational processes, while learning and growth OKR objectives could focus on the development of new skills and competencies.

By using the BSC as the basis for developing OKR objectives, an organization can ensure that its OKR sets cover a balanced range of objectives that support both short-term performance and long-term growth and innovation. The combination of BSC and OKR can thus improve the organization’s performance and lead to decisive competitive advantages.

Using BSC and OKR to get everyone working in the same direction and towards the same goal

The US manager and bestselling author (“The Five Dysfunctions of a Team”) summed up the importance of focus, alignment and coordination in the following quote: “If you could get everyone in an organization to row in the same direction, you could dominate any industry, in any market, against any competition, at any time.”

The alignment of all managers and employees towards common goals is of central importance for the success of a company. Team spirit and collective motivation are still often underestimated as the basis for successful performance. The use of BSC in combination with OKR enables and ritualizes precisely this ability to work together and promotes it systematically and significantly. Employees are encouraged to focus on the same goals and work in the same direction (top-down) – while at the same time having the freedom to set their own goals (bottom-up).

AUTHOR

- über 20 Jahre Experte in Digitalisierung, Strategie, OKR, Business Transformation und Innovation

- Praxiserfahrung und Mindset aus dem Silicon Valley für europäische Firmen adaptiert

- Rollen als C-Level-Führungskraft (u.a. bei ProSiebenSat.1), Startup Gründer und Unternehmensberater

- Keynote Speaker, Hochschuldozent und Bestseller Autor

- Gründer der DigitalWinners und der Marke OKR Experten®

Balanced Scorecard (BSC) FAQs

There are frequently recurring uncertainties about the balanced scorecard, which can often be easily clarified and resolved. Finally, the most frequently asked questions on the subject of BSC will be answered.

Is a balanced scorecard suitable for start-up companies?

Start-ups face the major challenge of integrating into and surviving in a dynamic business environment. Effective planning and implementation of the strategy is key to pursuing and achieving goals. A balanced scorecard also supports newly founded companies with the appropriate tools.

Is a balanced scorecard suitable for small companies?

The effective use of a balanced scorecard is not limited to resource-rich companies. The system can also be beneficial for small companies. A clear strategic orientation is relevant for every company. The structured planning capability of the BSC helps companies to define goals and make optimum use of their resources. This is possible regardless of their size.

How can a balanced scorecard be introduced in a company?

The effective use of a balanced scorecard is not limited to resource-rich companies. The system can also be beneficial for small companies. A clear strategic orientation is relevant for every company. The structured planning capability of the BSC helps companies to define goals and make optimum use of their resources. This is possible regardless of their size.

How can a balanced scorecard be introduced in a company?

A balanced scorecard can be introduced into a company using the seven-step plan:

- Strategic corporate goals

- Perspectives

- Goals for the perspectives

- Key figures for the prospects

- Target and threshold values for the key figures

- Visualization of the scorecard

- Implementation of the scorecard

The use of a template is also suitable.

What is a balanced scorecard framework?

A framework provides a conceptual template in connection with the balanced scorecard. It visualizes the overarching principles of the BSC.

Is the Balanced Scorecard useful in today’s world?

The Balanced Scorecard was developed at the beginning of the 1990s by the economists Robert S. Kaplan and David P. Norton. Since then, it has proven to be a highly innovative and useful tool for improving performance and modifying numerous industries. It makes it possible to create a multidimensional overall impression of the company’s performance. This makes the balanced scorecard a modern management system in strategic management.

What is a “Balanced Scorecard Strategy Map”?

A strategy map is a visual representation of a company’s vision and strategy. In a scorecard, it serves to make the perspectives, key figures and other values communicable and comprehensible.

How can a balanced scorecard be used to improve a company?

In order to use the balanced scorecard as effectively as possible, it must be firmly integrated into the management of a company. This can be achieved with the help of the seven-step plan outlined above.

Which system makes more sense: the BSC or the PEST analysis?

This decision depends on the specific requirements and ambitions of a company. PEST is an acronym for “Politics”, “Economy”, “Society” and “Technology”. It supports companies in analyzing external influences in the four areas mentioned.

Which software is suitable for creating a balanced scorecard?

The names of the most common and popular software for creating and managing a BSC are:

- BSC Designer

- QuickScore

- ClearPoint Strategy

- Spider Strategy

- Microsoft Excel

How can the Balanced Scorecard and OKR be combined?

The four perspectives of the Balanced Scorecard: financial perspective, customer perspective, internal process perspective and learning and growth perspective can be used very well to create and define holistic, high-quality and balanced OKR targets.

For example

- the financial perspective for the definition of sales growth or profit margins

- the customer perspective for customer satisfaction or market conquest objectives

- the process perspective for targets to improve specific operating processes

- the learning and development perspective for the objectives of developing new skills and competencies

inspire.

Related articles:

- https://hbr.org/1992/01/the-balanced-scorecard-measures-that-drive-performance-2

- https://hbr.org/2005/07/the-balanced-scorecard-measures-that-drive-performance

- https://www.researchgate.net/publication/309818479_Multi-level_strategic_alignment_within_a_complex_organisation

- https://en.wikipedia.org/wiki/Balanced_scorecard